Labour Market Weakness Calls for Continued Monetary Accommodation

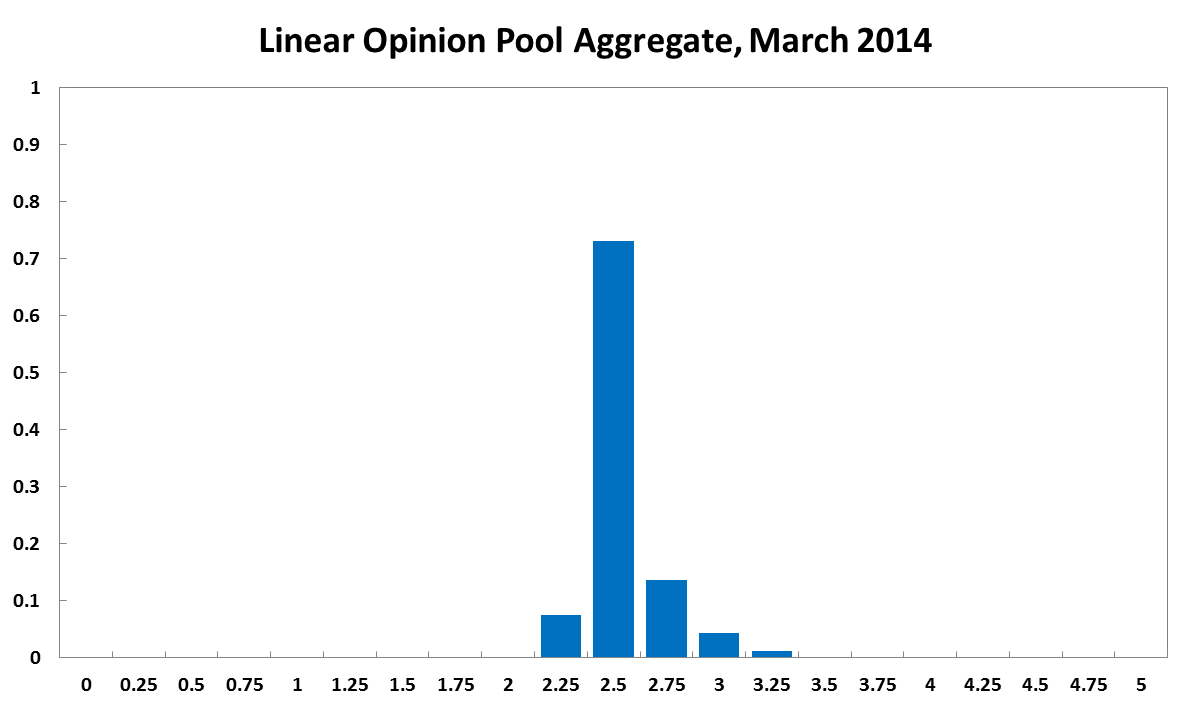

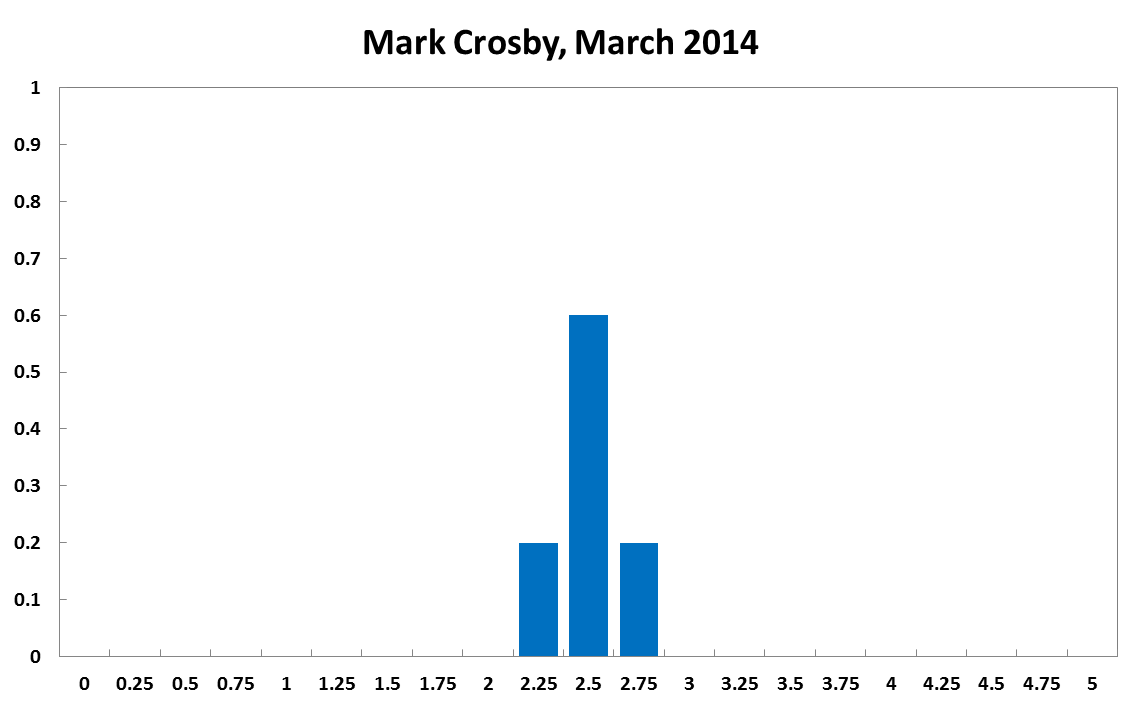

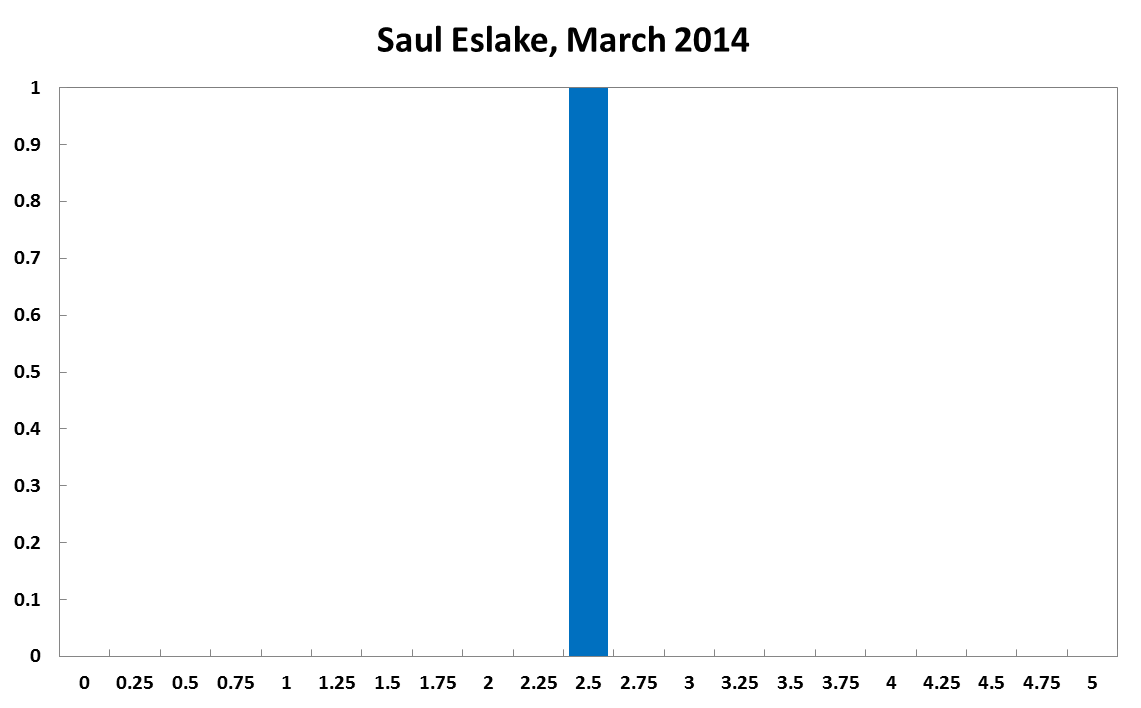

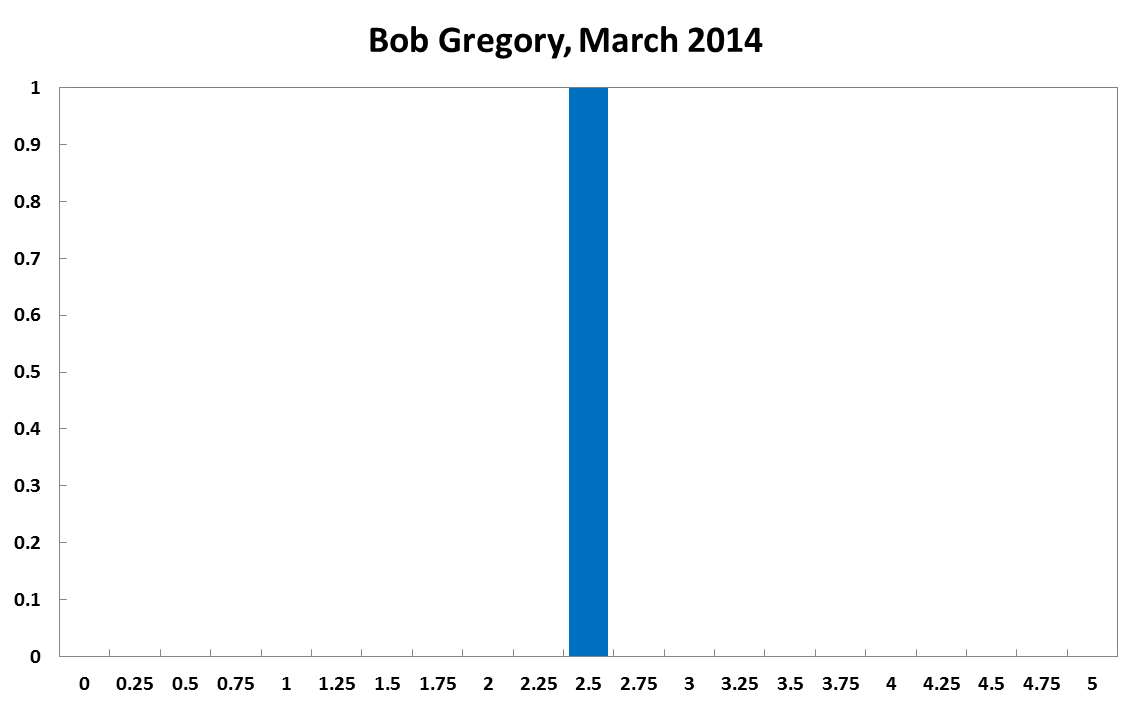

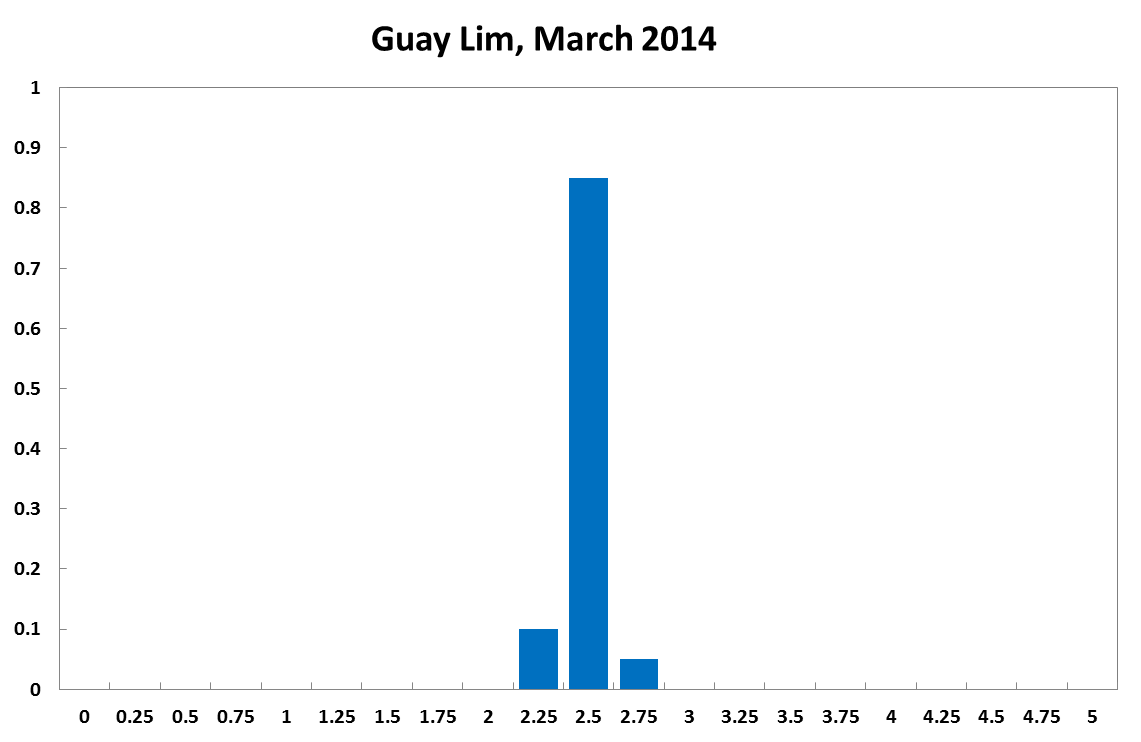

Weakness in the Australian labour market is making the CAMA RBA Shadow Board advocate continued monetary accommodation. The Shadow Board is 73% confident that the cash rate should remain steady at 2.5%. The probability attached to a required rate cut equals 8% while the probability of a required rate hike has fallen to 19%.

The Australian unemployment rate rose to 6% in January 2014, with underemployment and the median duration of unemployment also worsening. The key question is whether improvements in domestic demand will curb the increase in un- and underemployment or whether weakness in the labour market will persist.

Inflation has edged up but remains within the 2-3% target range. The Australian dollar has rebounded slightly from its recent lows to approx. 90 US cents. Asset markets, in particular housing, remain buoyant, bolstering the concern that it is cheap money, not sound fundamentals, that is driving asset prices.

Overseas, the picture is much the same as in the previous month. US economic data is still mixed but improving. Investors will closely scrutinize the new Federal Reserve Board governor’s rhetoric to identify any change in policy stance. The spectre of deflation is rearing its head in the Euro zone while major developing economies, especially the BRICS countries, continue to weaken. Global economic weakness may help to put a floor on the Australian dollar as international investors are looking for safe havens unless commodity prices plummet.

The consensus to keep the cash rate at its current level of 2.5% has increased further. The Shadow Board’s confidence in keeping the cash rate steady equals 73% (68% in February 2014). The probability attached to a required rate cut equals 8% (3% in February) while the probability of a required rate hike has fallen to 19% (28% in February).

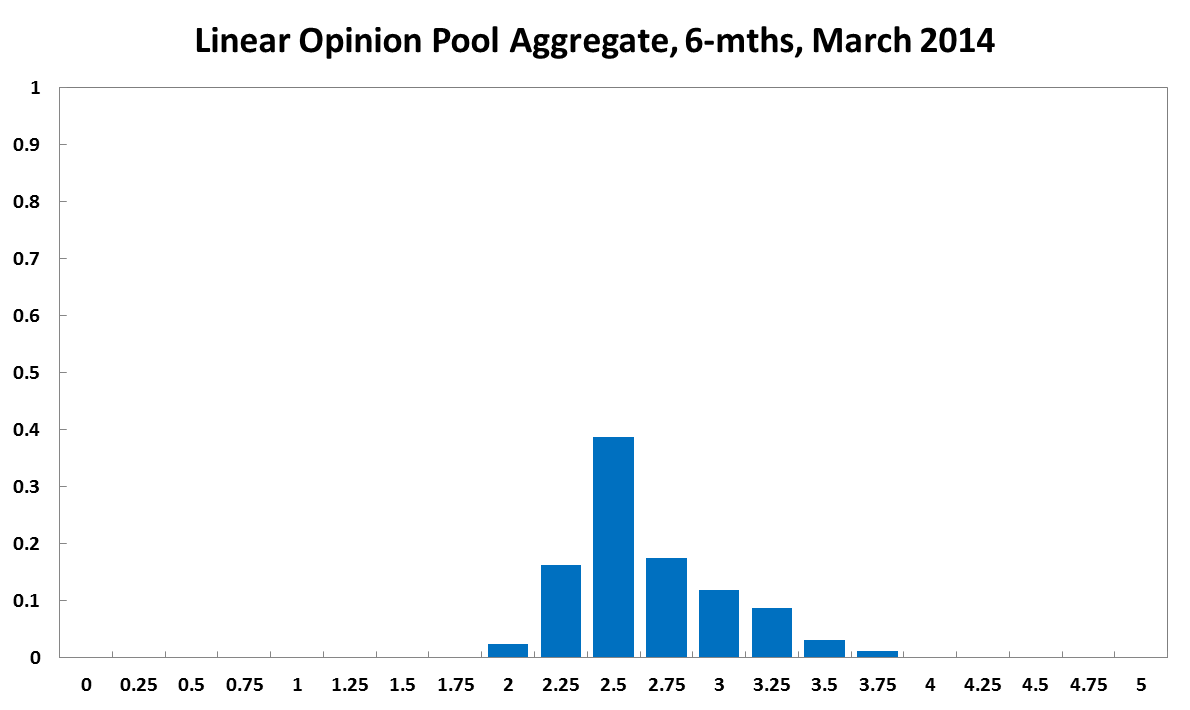

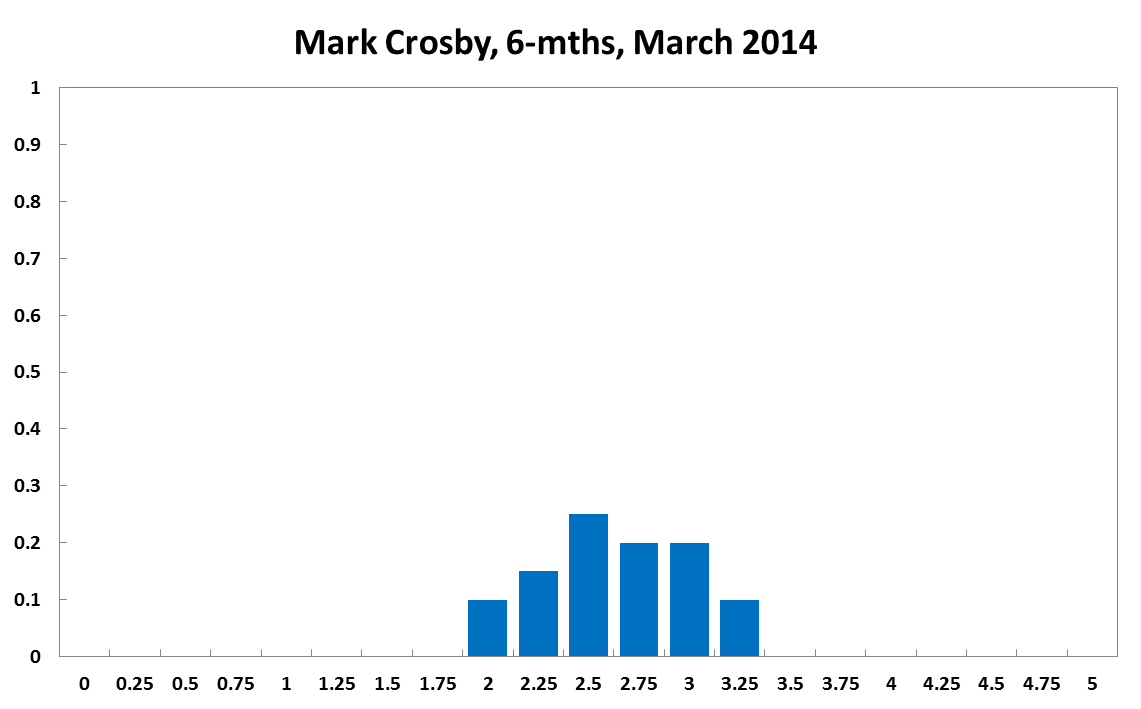

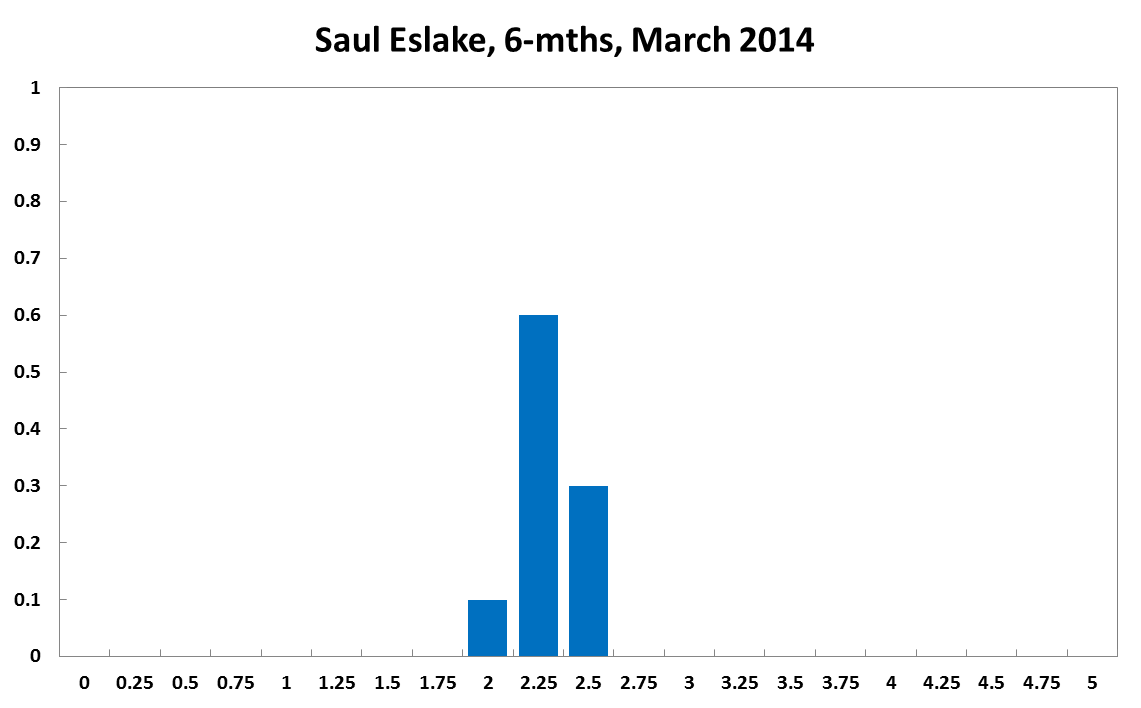

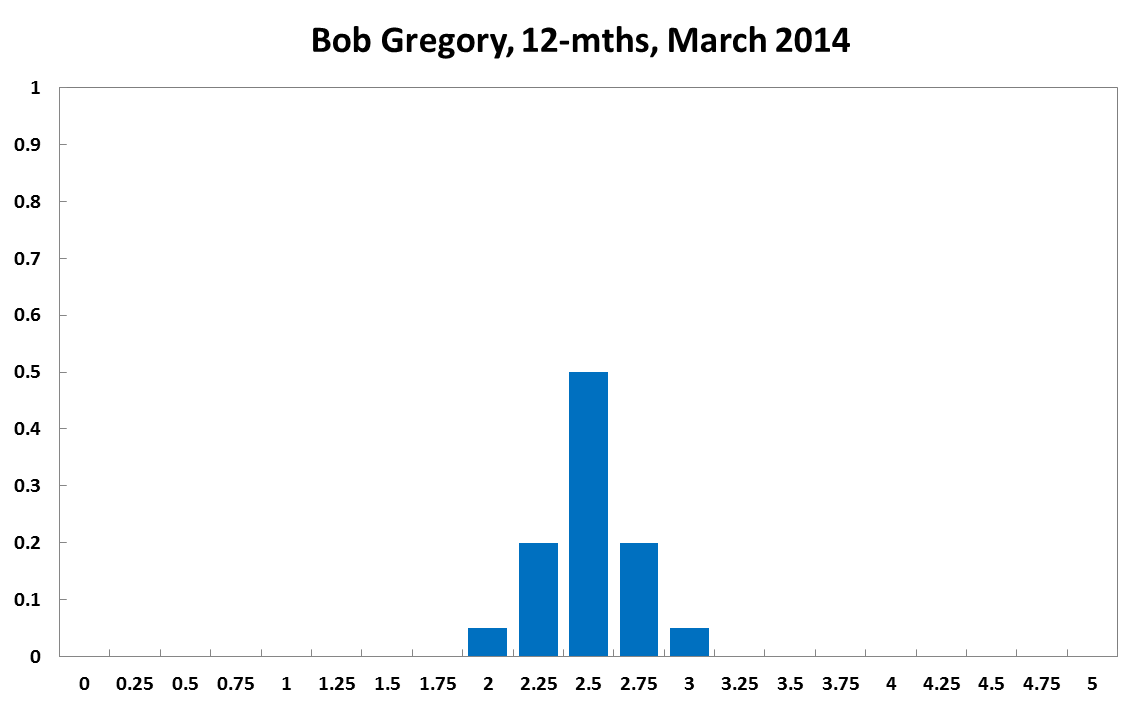

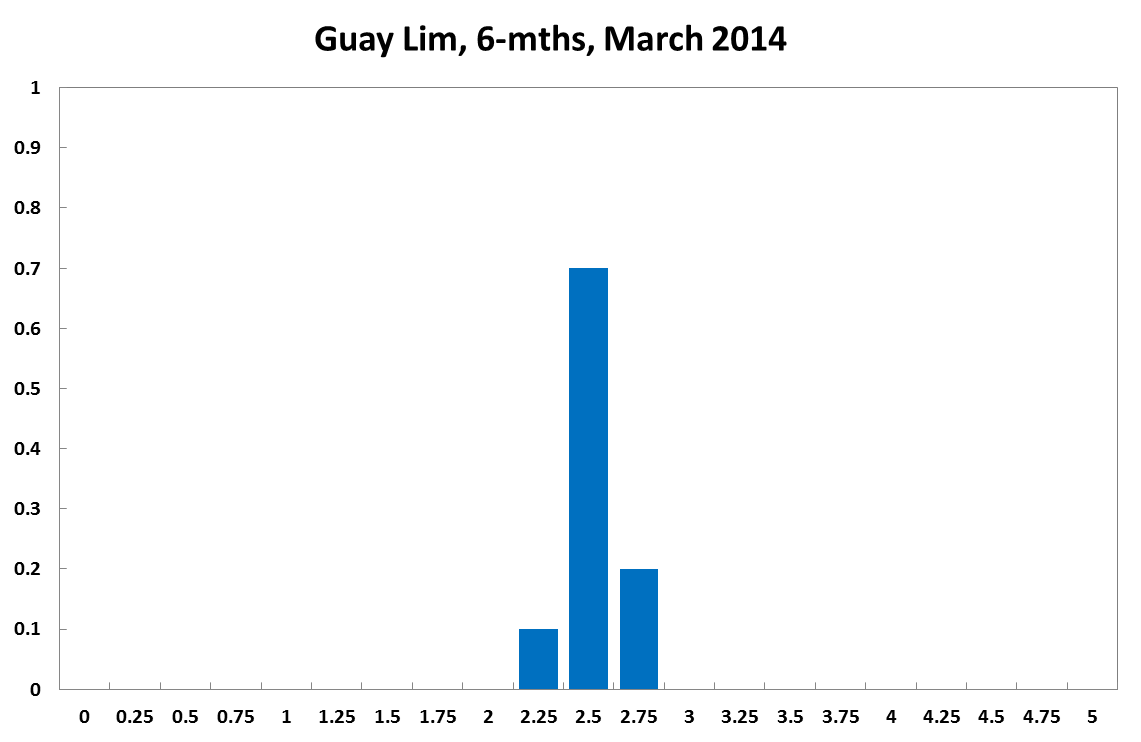

The probabilities at longer horizons are as follows: 6 months out, the probability that the cash rate should remain at 2.5% is unchanged at 39%. The estimated need for an interest rate increase is down a percentage point to 43%, while the need for a decrease has nudged up to 19% (17% in February). A year out, the Shadow Board members’ confidence in a required cash rate increase has fallen to 54% (58% in February), the need for a decrease remains unchanged at 19%, while the probability for a rate hold has risen to 26% (up from 23% in February).

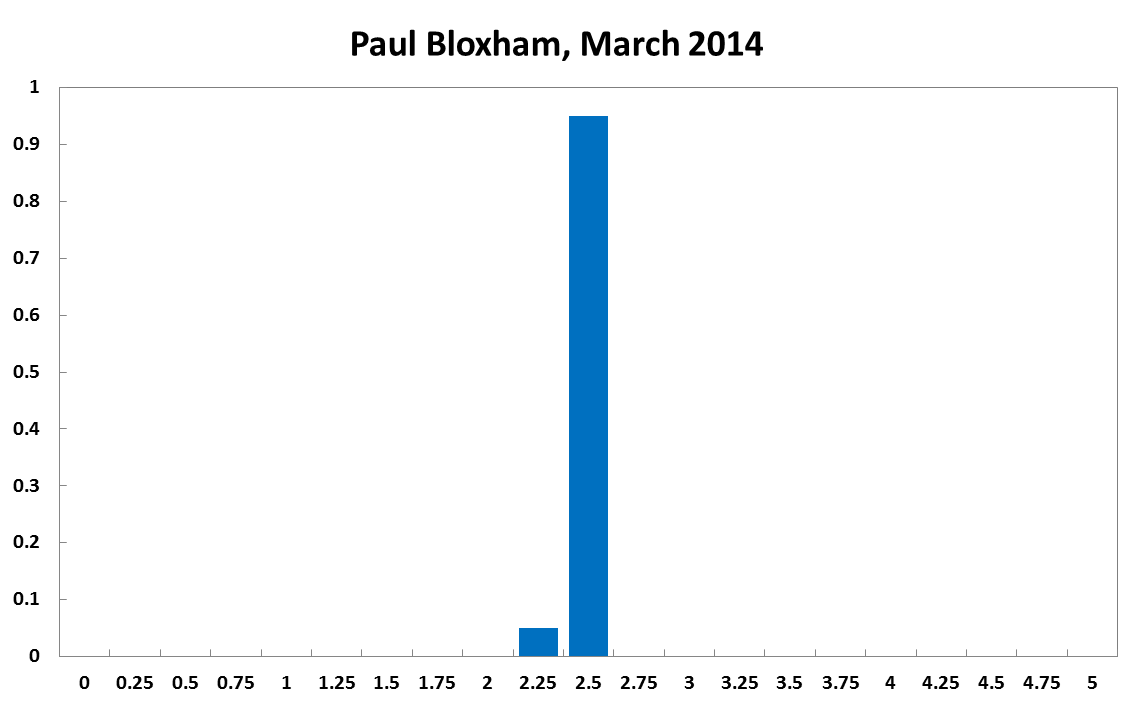

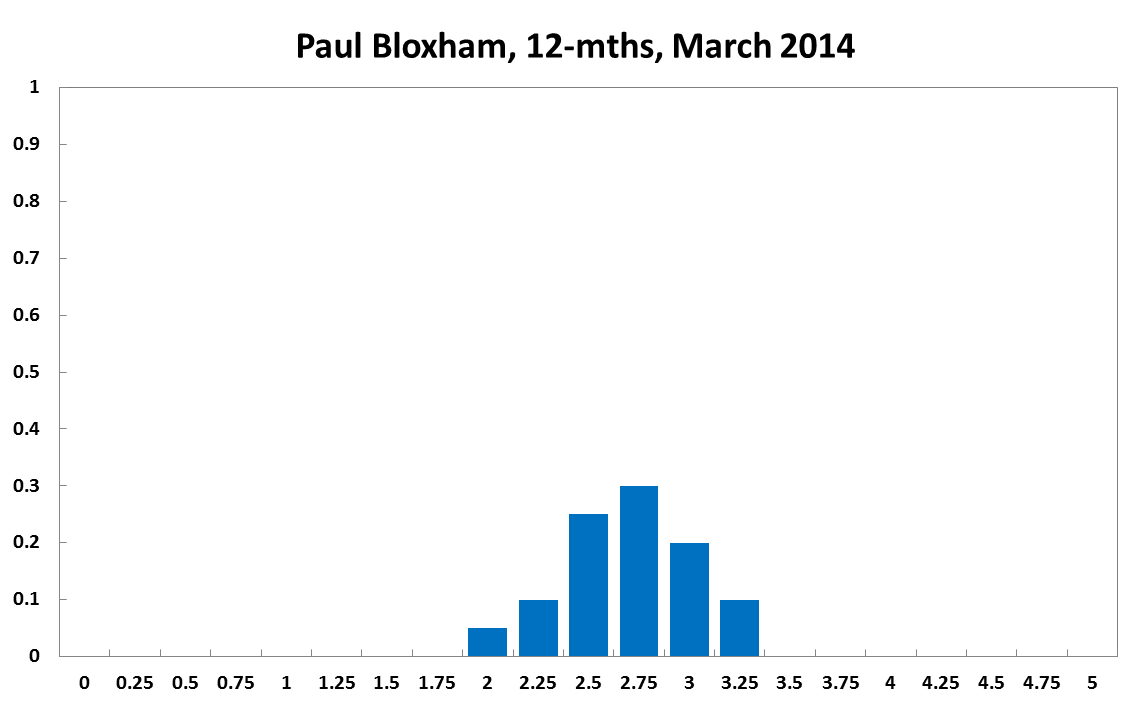

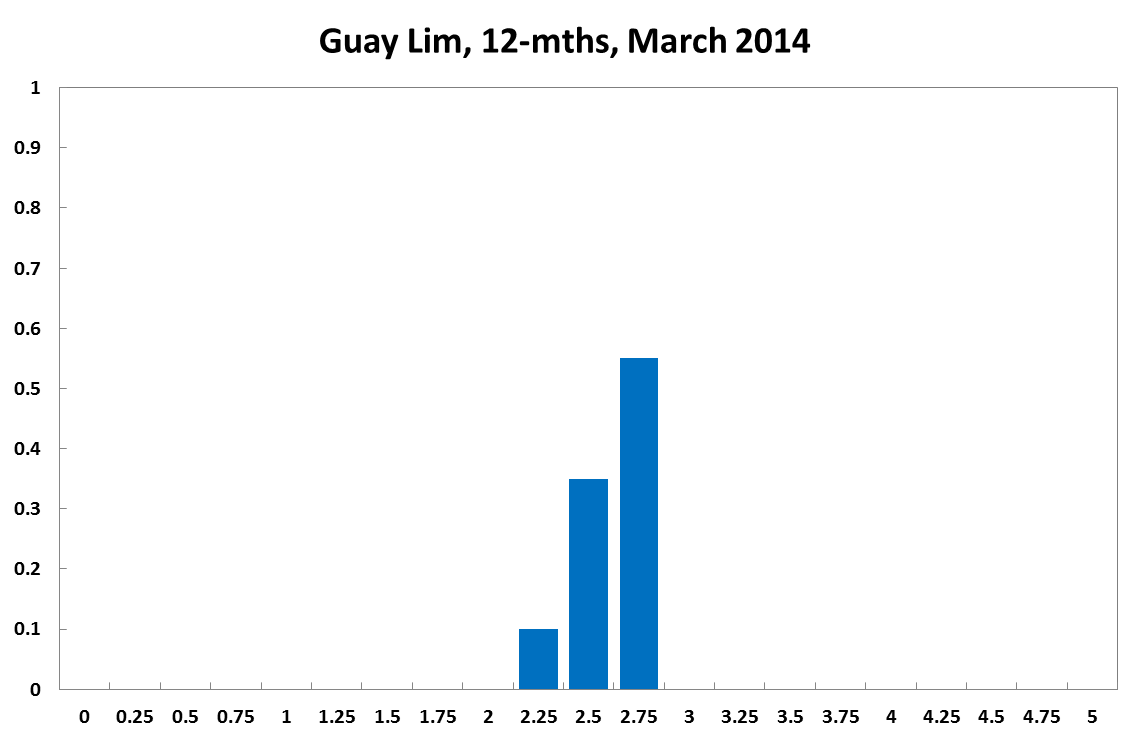

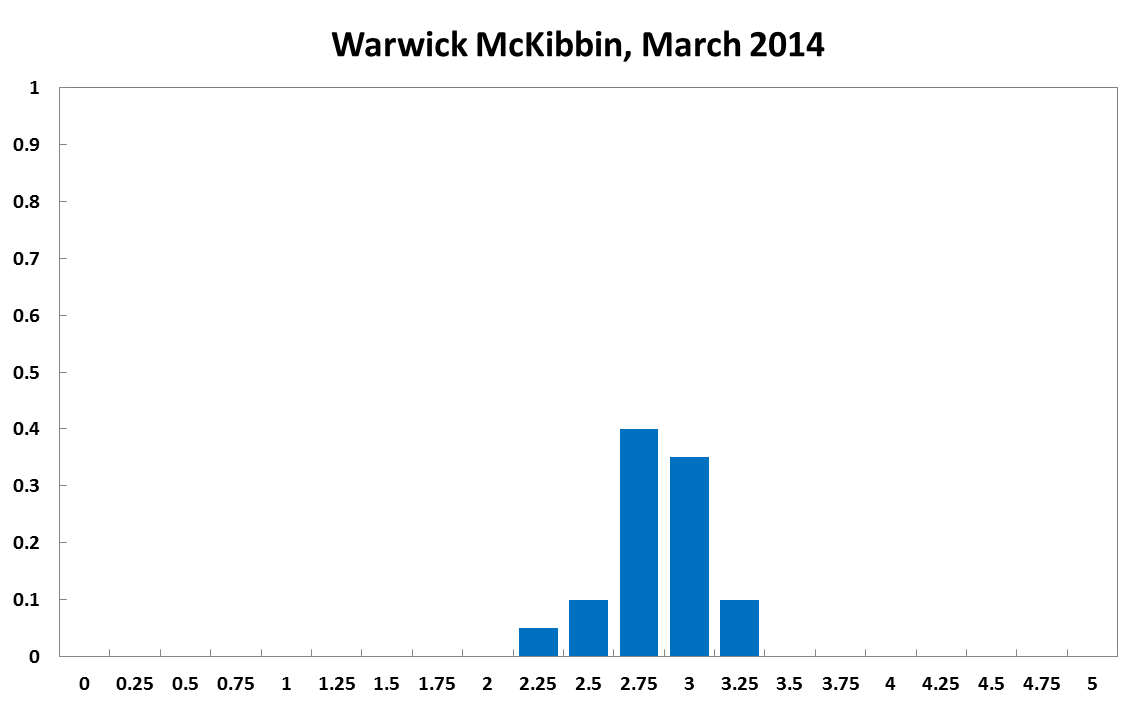

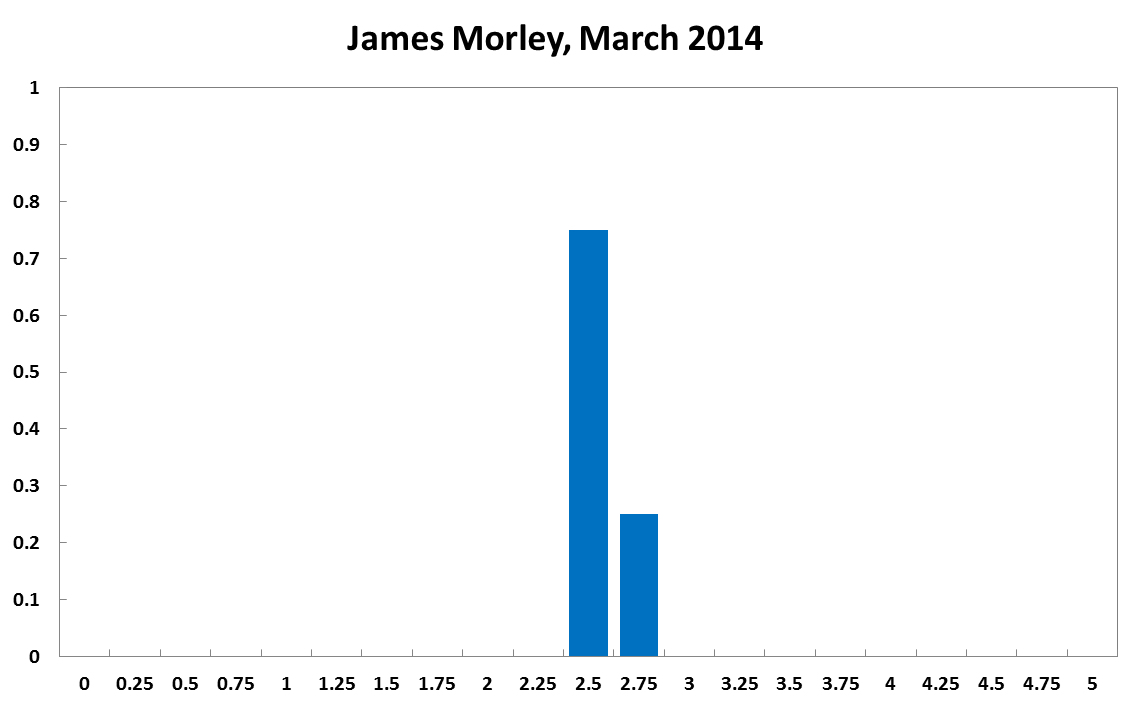

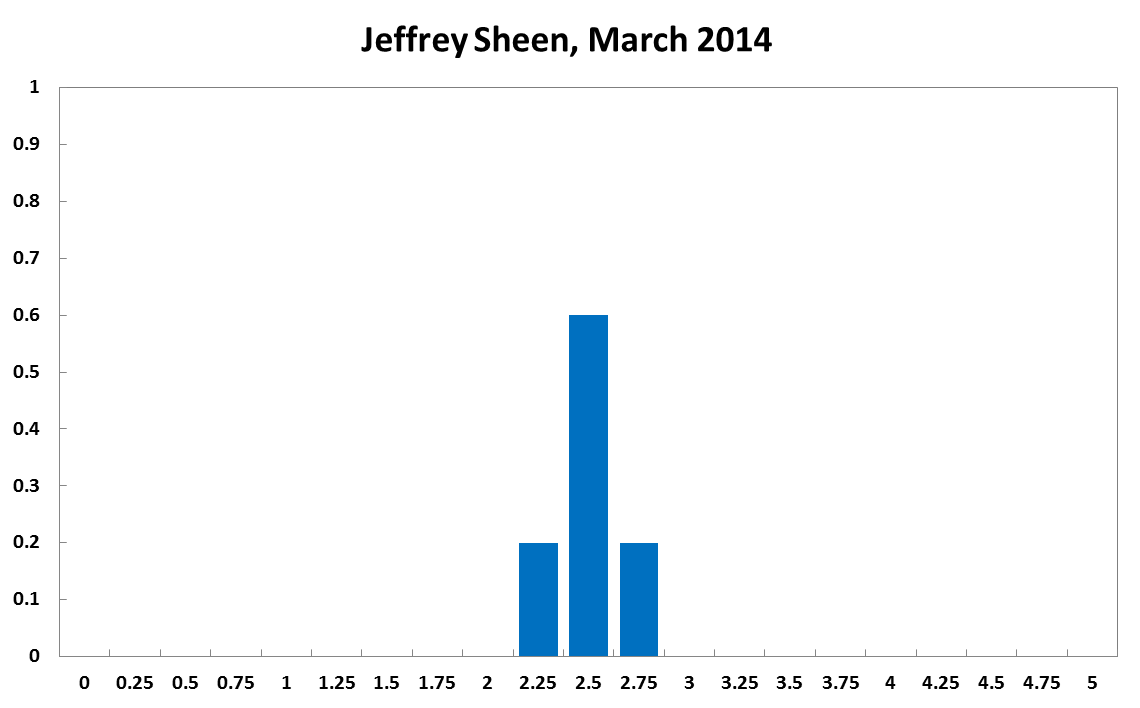

Note: Prof. Mardi Dungey was unable to vote in this round, so the linear opinion pool aggregate is based on 8 members.