Whither the Aussie Dollar?

Since the RBA dropped the cash rate to 2.75 percent last month the Australian dollar has fallen to below 96 US cents, a depreciation of more than 7 percent against the US dollar. With weaker data coming from China, India and Europe and mixed data coming from the US, the rapid fall in the Aussie dollar highlights the downside risks to the Australian economy, as perceived by the markets. Will the dollar slide further in anticipation of mounting downside risks, or will the current level suffice to boost Australian exports and breathe new life into the Australian economy?

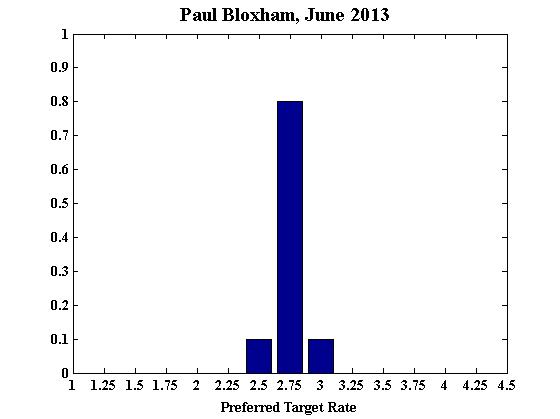

The tug-of-war between the need to lower the cash rate due to sustained weakness in the Australian economy and the need to raise the cash rate in response to the expansionary stimulus emanating from the historically low cash rate and the weakened Aussie dollar, is clearly on the minds of the shadow board members.

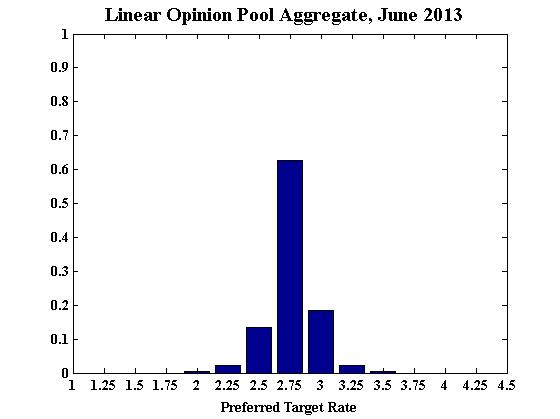

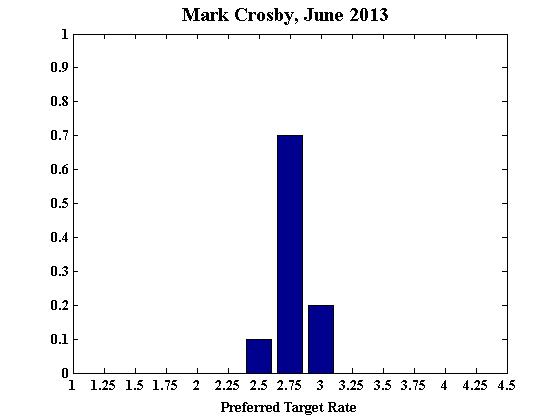

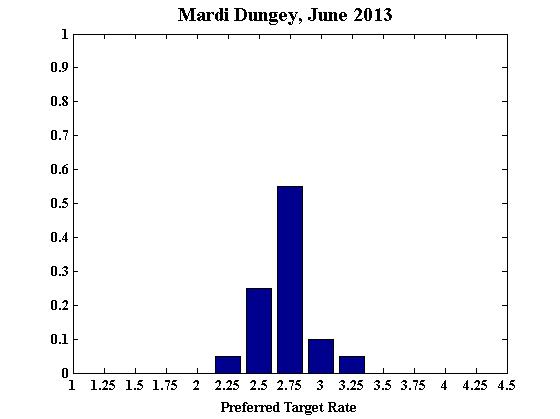

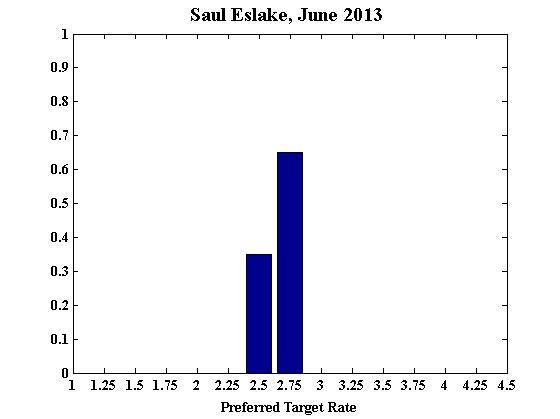

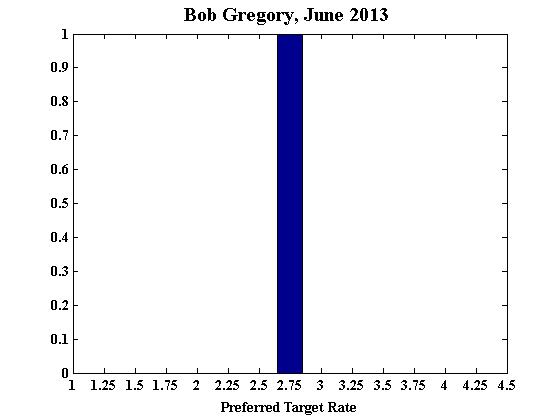

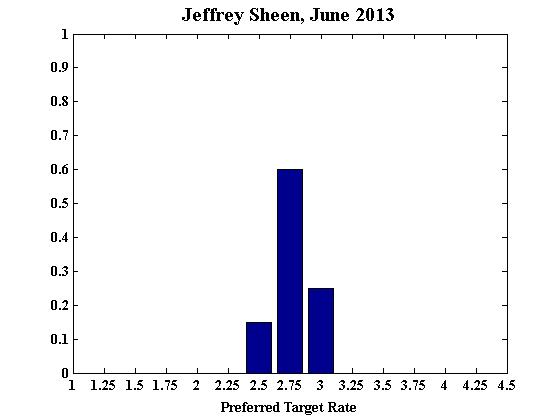

The strong consensus of the nine members is that the Reserve Bank of Australia should leave interest rates unchanged from May at 2.75 percent.

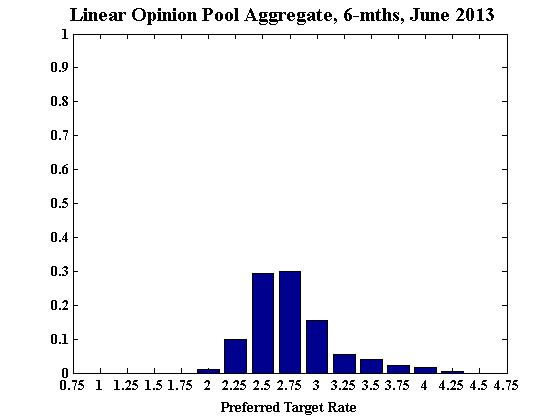

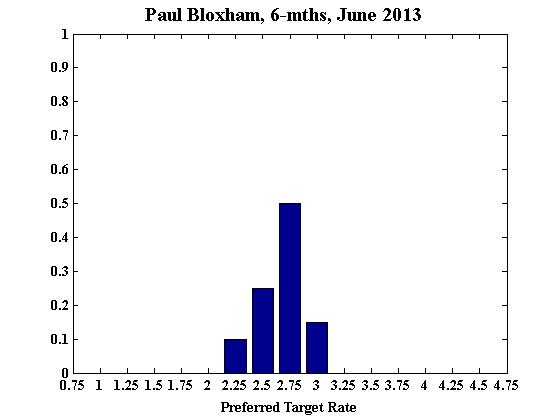

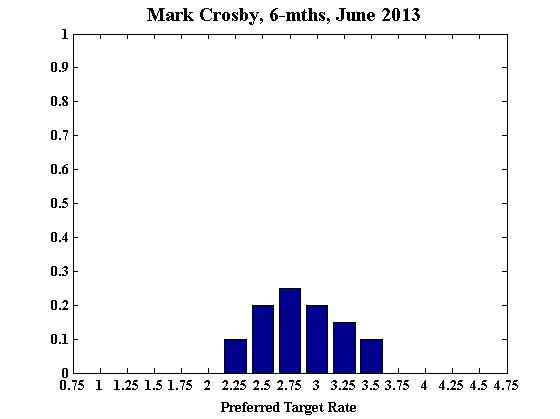

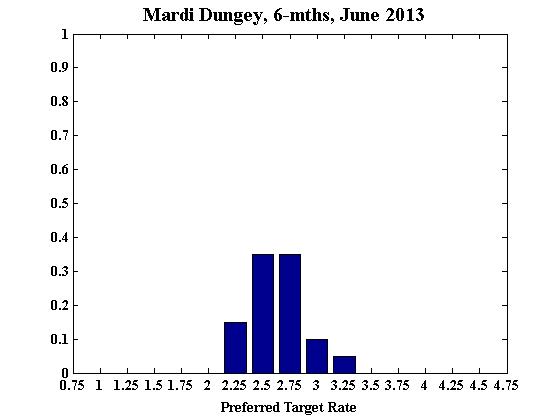

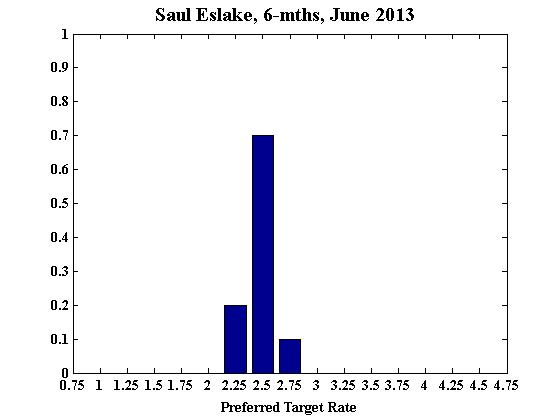

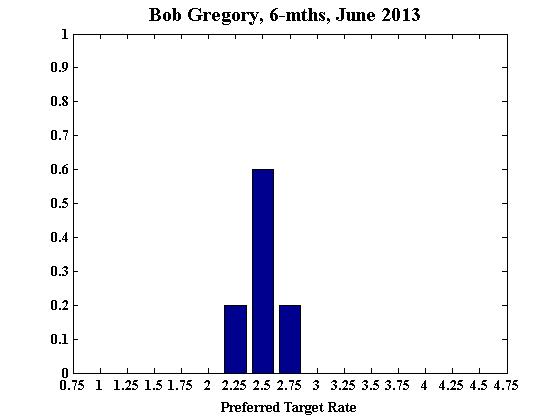

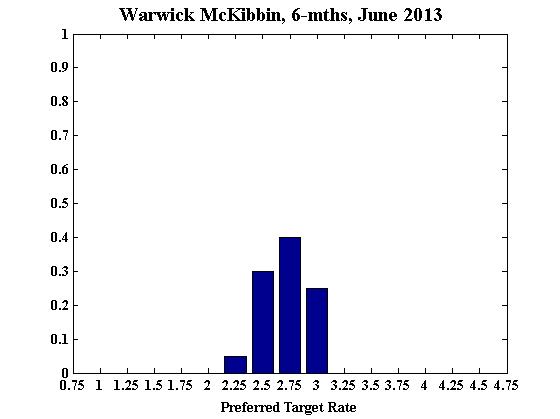

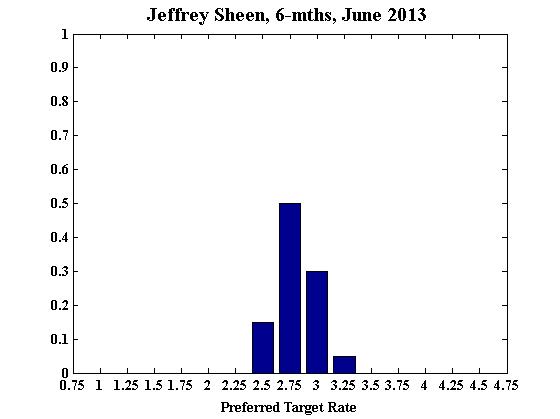

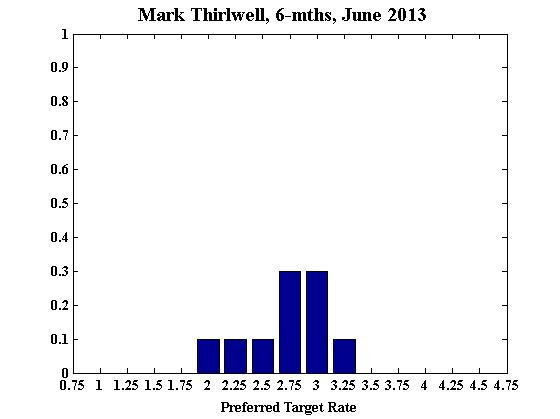

The probability that rates should rise in the next six months equals approx. 1/3, somewhat less than the risk that rates should be lower.

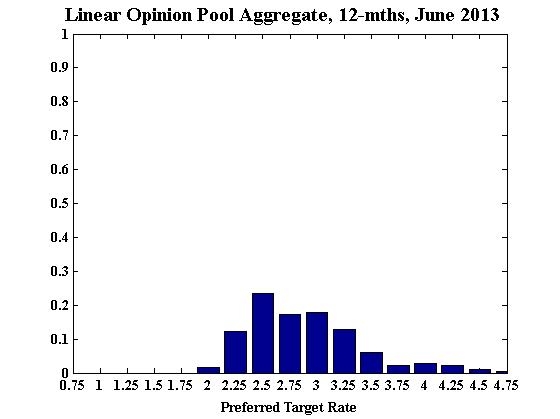

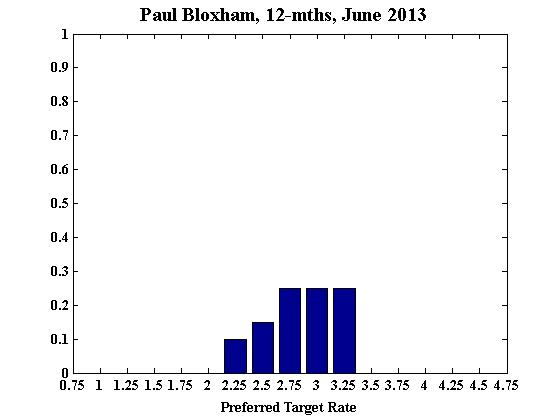

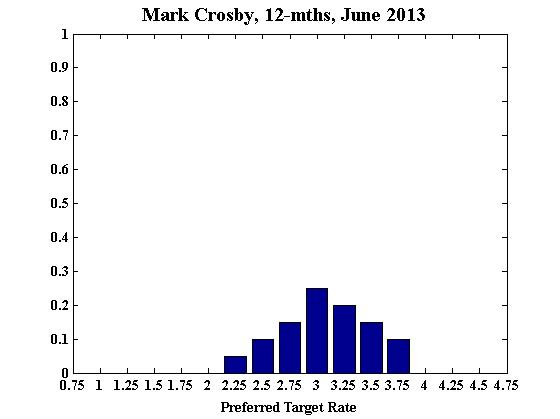

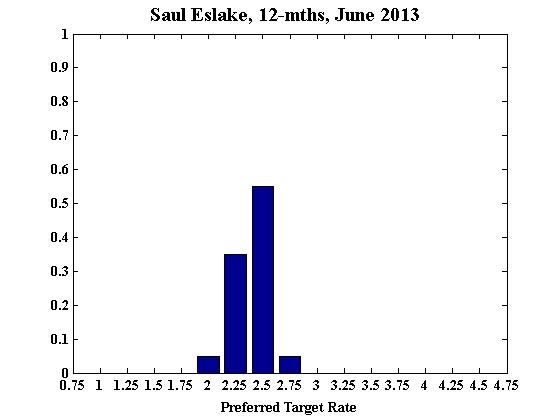

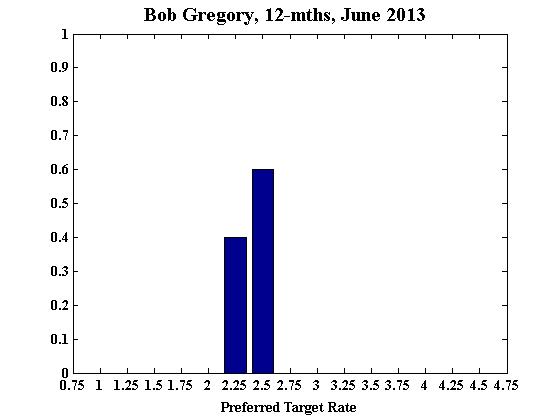

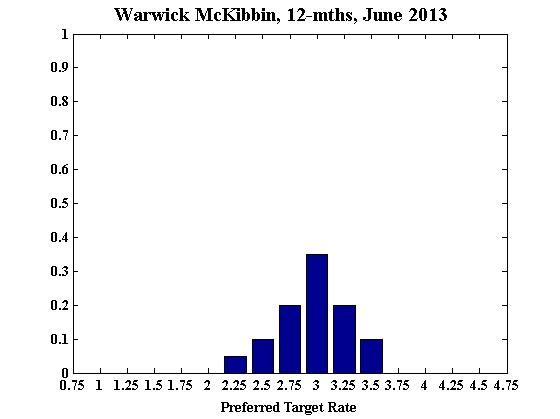

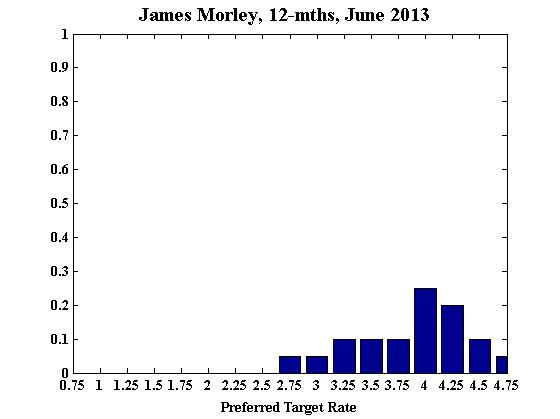

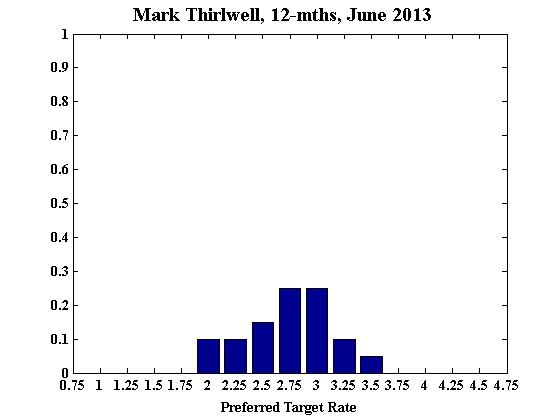

Over the longer term, in the next twelve months, the Shadow Board members anticipate that the probability of a rate increase is around 40 percent, slightly more than the probability of a fall. Overall, compared to previous months, there has been a small shift in favour of lower interest rates at the 6-month and 12-month horizon, reflecting concerns about muted consumption, weaker global demand, falling commodity prices and tighter fiscal policy following a likely change of government later this year.